If you have invested in Certificates of Deposits before, you know that CDs are safe investments with higher interest rates than regular savings accounts. Yet, CDs can be restrictive due to their set maturities. When you buy a CD, you can’t withdraw the money before it matures without paying a penalty. To overcome this drawback, experienced investors don’t put all their money into one CD. Instead, they invest through a CD ladder. In this article, we will teach you how to build the perfect CD ladder.

What is a CD ladder?

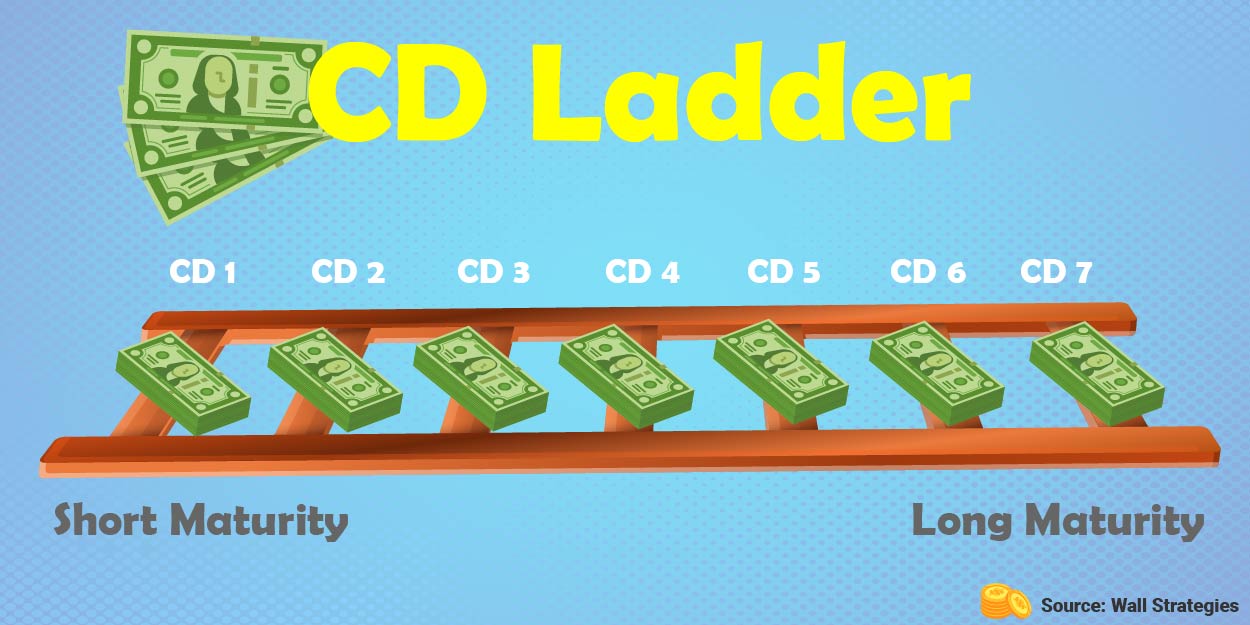

A CD ladder is a portfolio of individual Certificates of Deposits with different maturities. Typically, the maturities are evenly spread out. For example, you can have a CD ladder with one year between maturities. When you plot their maturity dates, it looks like a ladder, hence the name – CD ladder!

CD Ladder example

Let’s go through a CD ladder example. Suppose you have $15,000 to invest in CDs. After looking at the prevailing interest rates for each maturity, you like 3-year CDs the best. Without a ladder, you will have to put all $15,000 into a 3-year CD. This is a lump sum investment and it has a few drawbacks. First, a lump sum investment locks up all your money until maturity. This gives you little flexibility to withdraw your money when you need to. Second, if the interest rate goes up in the next two years, a lump sum investment does not allow you to take advantage of the higher interest rate.

To overcome these drawbacks, you can build a 3-year CD ladder. First, you divide the principal into three $5,000 investments. Then invest $5,000 in a 1-year CD, another $5,000 in a 2-year CD, and the rest in a 3-year CD. Now you have a CD ladder that looks like this:

| CD Ladder Example | CD 1 | CD 2 | CD 3 |

| Amount | $5,000 | $5,000 | $5,000 |

| Maturity | 2021 | 2022 | 2023 |

How does a CD ladder work?

Every time a CD matures, you reinvest the money back into another three-year CD and keep extending the ladder. In our example, the first CD matures next year and you can then invest the money into another 3-year CD. The reinvestment process ramps up the overall maturity and return of your CD ladder.

- In 2021, CD 1 matures and is reinvested into a 3-year CD that matures in 2024.

- In 2022, CD 2 matures and is reinvested into a 3-year CD that matures in 2025.

Here is the interesting part: after two years, the first two CDs have matured and the money is reinvested in new 3-year CDs. Now all of your money is invested in 3-year CDs, earning higher interest rates! Moreover, because the maturities are evenly spaced out, every year a portion of your investment will become available for use or reinvestment.

The benefits of CD ladders

The biggest benefit of a CD ladder is that it lets you enjoy the high interest rates of long-term CDs without locking down all your money. Without a ladder, you will have to lock up all your money for three-years to earn a higher interest rate. Because CDs come with early withdrawal penalties, putting all your money in one long-term CD is risky and inconvenient.

On the other hand, using a CD ladder is a smart way to gradually build up a portfolio of long-term CDs while keeping the money accessible. In our example, after the first two years, you will build up a portfolio of 3-year CDs. However, because the CDs mature one after another, each year you will unlock a portion of your investment. This flexibility is valuable.

A CD ladder gives you an opportunity to benefit from rising interest rates. Let’s assume a scenario where the interest rate goes up in two years. If you have invested all your money into a three-year CD, the interest rate is locked for three years and you won’t be able to benefit from the higher interest rate. However, with a ladder, you will receive a portion of your investment every year. This allows you to reinvest with a higher interest rate.

When you might use CD ladders

CD ladders are helpful tools to save for recurring expense and they help you plan ahead! For example, you can set-up a CD ladder to pay for college tuition by aligning CD maturities with tuition payments.

How to build a perfect CD ladder?

A well-planned CD ladder gives you safety, regular income, and flexibility. There are many ways to build an effective CD ladder. To find one that works for your saving goals, you need to consider two factors.

Target Maturity – your target maturity depends on what kind of CDs you want to invest in after the ladder ramps up. In our example, we want to invest in 3-year CDs, so three-year is the target maturity. If you find five-year CDs more attractive, you can use that as your target.

Investment Interval – this is the gap between two CD maturities. In our example, the gap was one year. In practice, the interval depends on how often you need the money. For example, if you are investing the money to pay for college tuition, you can choose 6 months as your interval. If you need access to some of your money every year, you should keep the maturities one year apart from each other.

Should I use a CD ladder?

Investing is a personal experience. Your investment strategy has to work for you and your goals. While CD ladders are useful, you should first check if CDs are the best investments for you. For example, if you have a high income, you might want to consider investing in municipal bonds instead of CDs, because muni bonds can reduce your federal and state tax obligations.

But if you are already familiar with CDs and their restrictions, using a CD ladder can enhance your investment experience!